Project Description

Entrepreneurship and digital finance

The Blockchain Research Lab looks to assess entrepreneurial opportunities arising from blockchain technology, such as startup financing in the form of Initial Coin Offerings (ICOs) or security tokens.

While the potential of blockchain-based financing is great, the market is still immature. Therefore, the Blockchain Research Lab launched a project to gain further understanding of the phenomenons and related markets.

Publications:

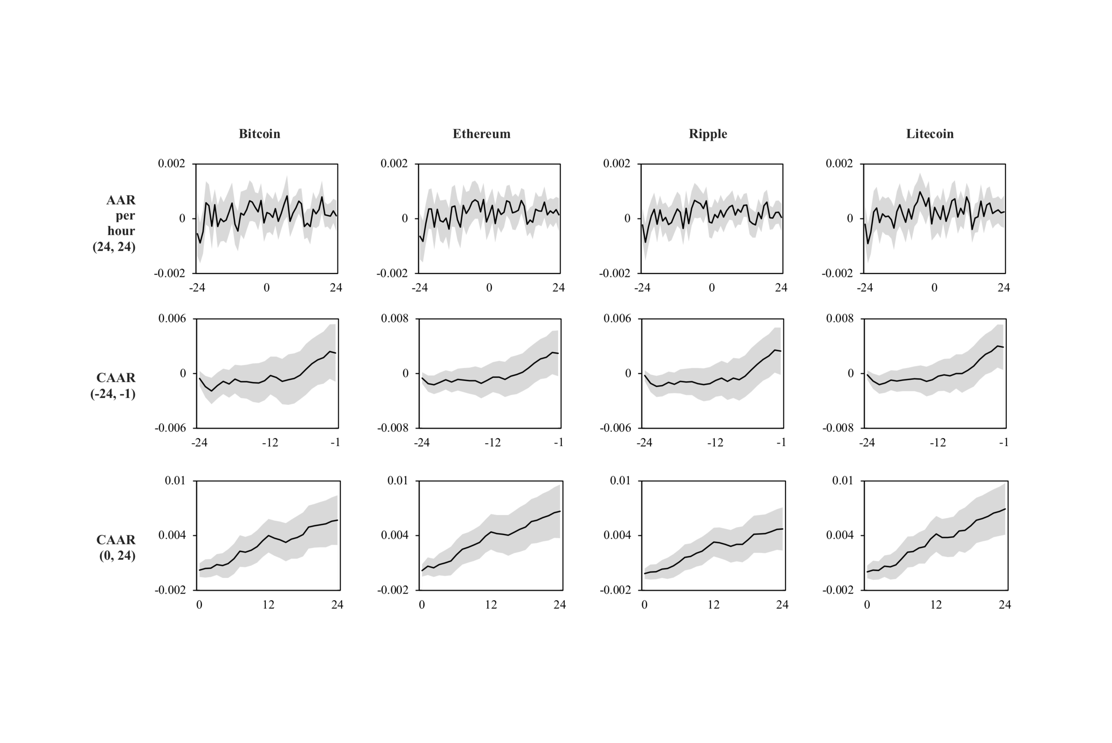

The Influence of Stablecoin Issuances on Cryptocurrency Markets

We analyze the influence of stablecoin issuances on the returns of major cryptocurrencies across 565 issuance events of $1 million or more for seven different stablecoins on four different blockchains between April 2019 and March 2020.

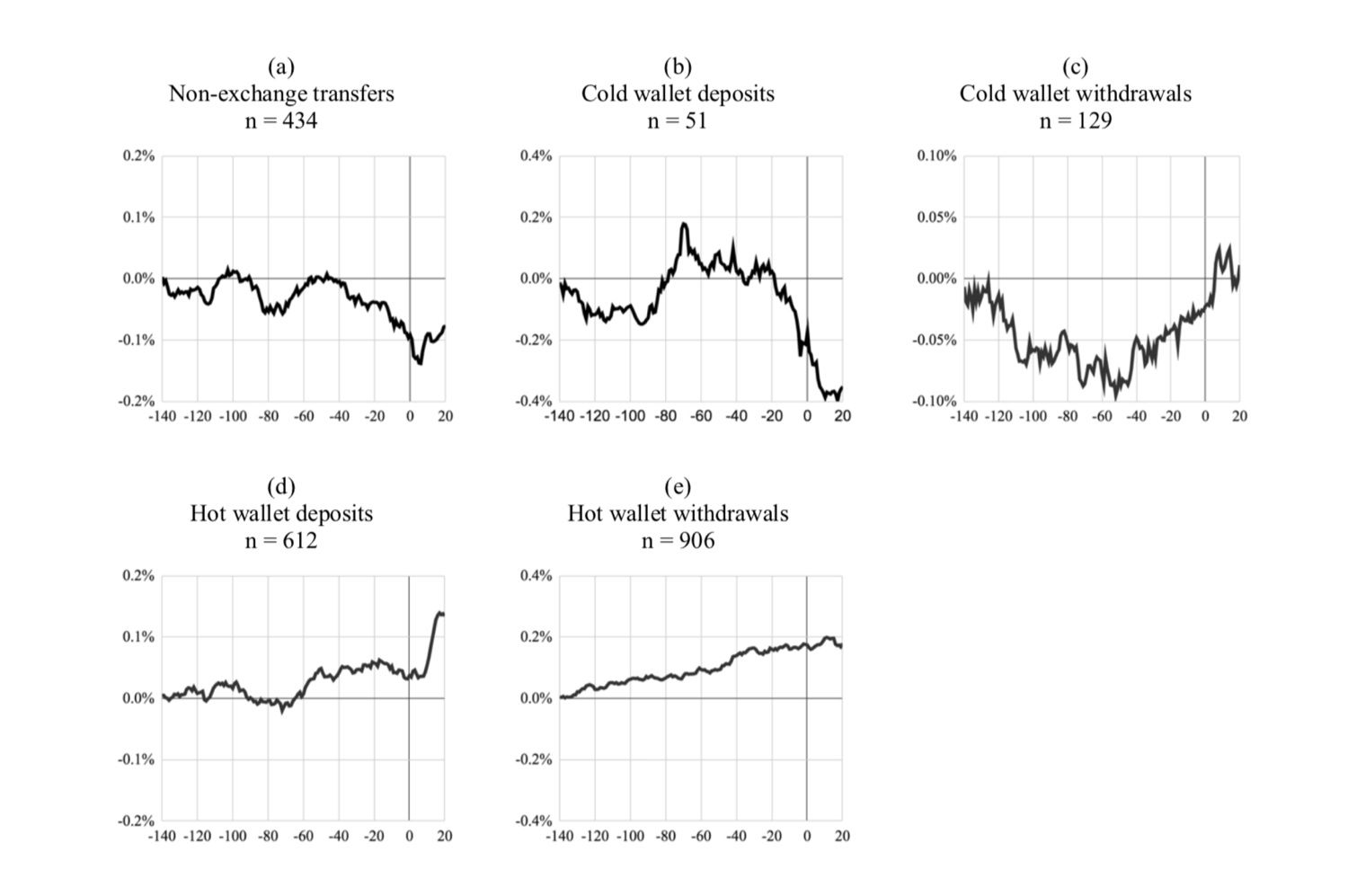

Market Reaction to Large Transfers on the Bitcoin Blockchain – Do Size and Motive Matter?

Cryptocurrency markets are often deemed inefficient. This paper explores how the market reacts to a specific form of public information: large Bitcoin transactions. The event study examines the price effects of 2,132 transactions involving at least 500 Bitcoins...

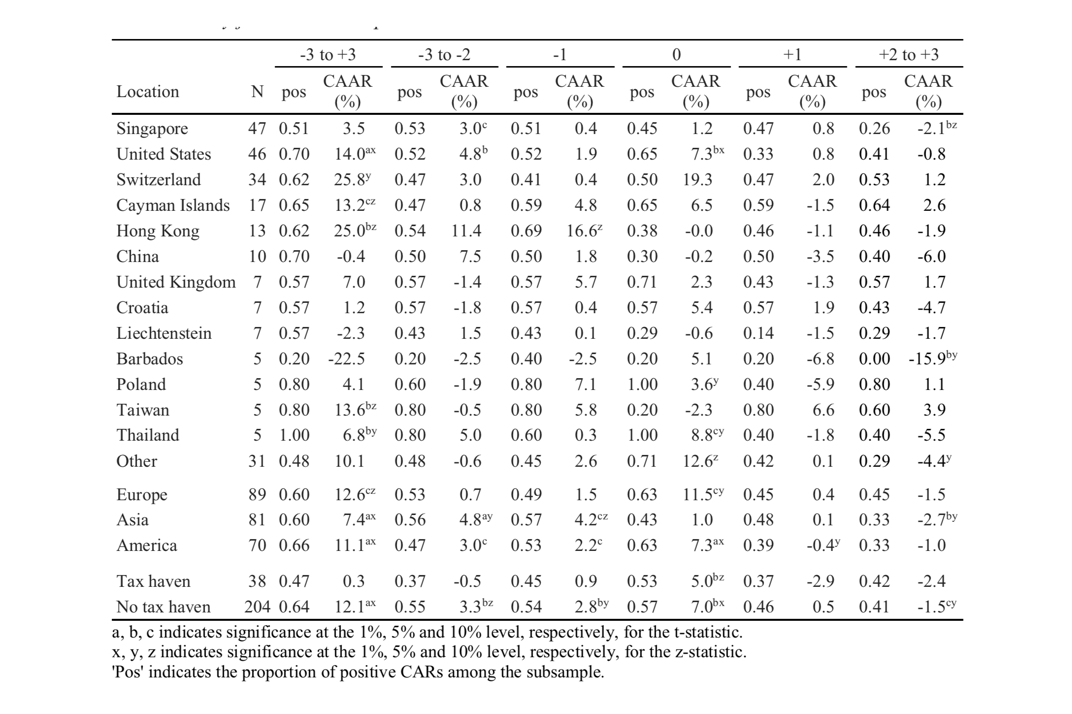

Effects of Initial Coin Offering Characteristics on Cross-listing Returns

This paper examines how initial coin offering (ICO) characteristics affect cross-listing returns, i.e. whether or not the available information is a valuable signal of quality. For this purpose, we analyze 250 cross-listings of 135 different tokens issued via ICOs and calculate abnormal returns for specific samples using event study methodology.